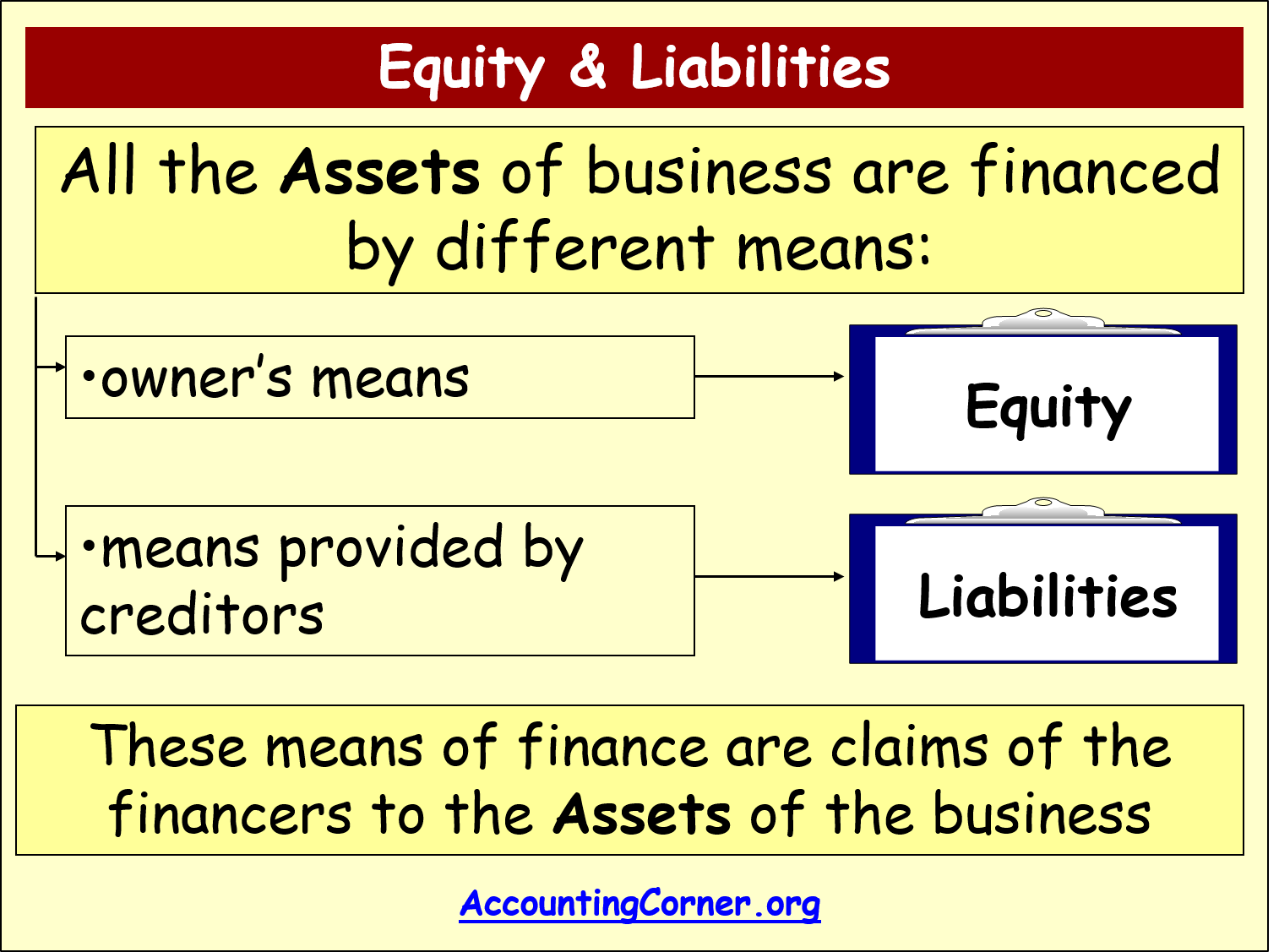

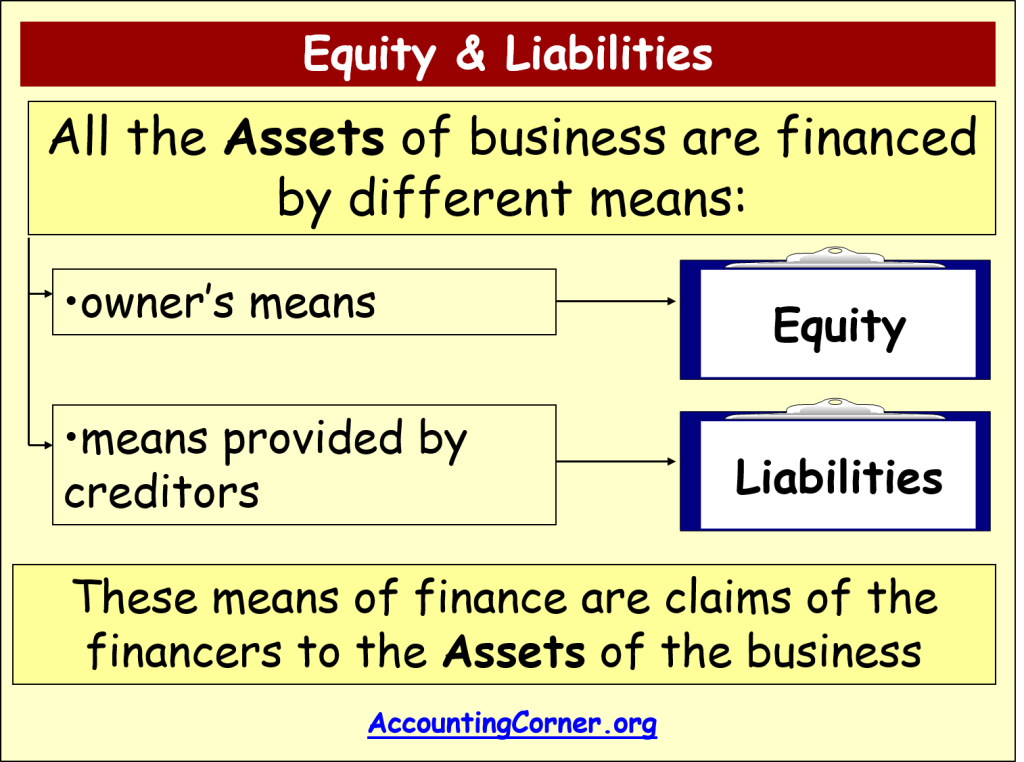

The accounting equation shows how a company’s assets, liabilities, and equity are related and how a change in one results in a change to another. In the basic accounting equation, assets are equal to liabilities plus equity. This straightforward relationship between assets, liabilities, and equity is the foundation of the double-entry accounting system. That is, each entry made on the Debit side has a corresponding entry on the Credit side. In above example, we have observed the impact of twelve different transactions on accounting equation. Notice that each transaction changes the dollar value of at least one of the basic elements of equation (i.e., assets, liabilities and owner’s equity) but the equation as a whole does not lose its balance.

Let us take a look at transaction #1:

The bank has a claim to the business building or land that is mortgaged. On 5 January, Sam purchases merchandise for $20,000 on credit. As a result of the transaction, an asset in the form of merchandise increases, leading to an increase in the total assets. As transactions occur within a business, the amounts of assets, liabilities, and owner’s equity change. The inventory (asset) of the business will increase by the $2,500 cost of the inventory and a trade payable (liability) will be recorded to represent the amount now owed to the supplier. In the above transaction, Assets increased as a result of the increase in Cash.

To Ensure One Vote Per Person, Please Include the Following Info

My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. An asset is a resource that is owned or controlled by the company to be used for future benefits. Some assets are tangible like cash while others are theoretical or intangible like goodwill or copyrights. The 500 year-old accounting system where every transaction is recorded into at least two accounts.

Ask Any Financial Question

- It can be found on a balance sheet and is one of the most important metrics for analysts to assess the financial health of a company.

- The major and often largest value assets of most companies are that company’s machinery, buildings, and property.

- Does the stockholders’ equity total mean the business is worth $720,000?

- Small business owners typically have a 100% stake in their company, while growing businesses may have an investor and share 20%.

- The 500 year-old accounting system where every transaction is recorded into at least two accounts.

One of the main financial statements (along with the balance sheet, the statement of cash flows, and the statement of stockholders’ equity). The income statement is also referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement. The owner’s equity is the balancing amount in the accounting equation. So whatever the worth of assets and liabilities of a business are, the owners’ equity will always be the remaining amount (total assets MINUS total liabilities) that keeps the accounting equation in balance.

As a result of this transaction, an asset (i.e., cash) increases by $10,000 while another asset ( i.e., merchandise) decreases by $9,000 (the original cost). The assets of the business will increase by $12,000 as a result of acquiring the van (asset) but will also decrease by an equal amount due to the payment of cash (asset). $10,000 of cash (asset) will be received from the bank but the business must also record an equal amount representing the fact that the loan (liability) will eventually need to be repaid. We will now consider an example with various transactions within a business to see how each has a dual aspect and to demonstrate the cumulative effect on the accounting equation. In the case of a limited liability company, capital would be referred to as ‘Equity’.

Previously, a non current asset used to be called a fixed asset. Largely because those assets tend to be “fixed” (e.g., buildings). Assets held for the long term are called “Non-current assets”.

11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. 11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. Finance Strategists why choose a career in accounting has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own. The merchandise would decrease by $5,500 and owner’s equity would also decrease by the same amount.

As this is not really an expense of the business, Anushka is effectively being paid amounts owed to her as the owner of the business (drawings). Therefore cash (asset) will reduce by $60 to pay the interest (expense) of $60. The cash (asset) of the business will increase by $5,000 as will the amount representing the investment from Anushka as the owner of the business (capital). Equity represents the portion of company assets that shareholders or partners own. In other words, the shareholders or partners own the remainder of assets once all of the liabilities are paid off. Incorrect classification of an expense does not affect the accounting equation.